The longest period of economic expansion in modern US history has just come to a crashing end, courtesy of the COVID-19 virus and a price war in the global oil markets. The global economy is seemingly grinding to a halt as more and more of the world is now adjusting to “shelter-in-place” mandates from governmental authorities, intended to slow down the spread of this virus. While clearly necessary, these actions are already having an enormous impact on the global economy. It is far too early to assess the magnitude of the economic damage being done, but it will be considerable. As an investor in emerging consumer goods companies, neither we at CircleUp, nor the entrepreneurs we have partnered with, are immune. Starting a new business is incredibly difficult at the best of times, and the current environment presents an existential crisis for many business operators. The challenge presented is especially acute given that much of everyone’s focus is – as it should be – on the health and safety of their family and friends. To put it bluntly: this will be an extremely difficult time for our entrepreneurs, their consumers, our LPs, and our company.

In this note, we would like to share with stakeholders across the CircleUp ecosystem our perspectives on the impact of this crisis on the consumer packaged goods (CPG) industry. We will summarize what we have seen thus far through the lens of the consumer-facing industries in which we invest, and share how we are working with current and prospective portfolio companies to get through this immensely difficult period.

Consumer packaged goods in a recession

At CircleUp, we primarily invest in emerging consumer companies with a focus on the branded consumer packaged goods sector. CPG products are typically low price point and high repeat purchase items that include the beverages we drink, the food we eat and feed to our pets, and the products we put on our skin and use to clean our homes. This puts the vast majority of the brands in which we invest in the consumer staples sector.

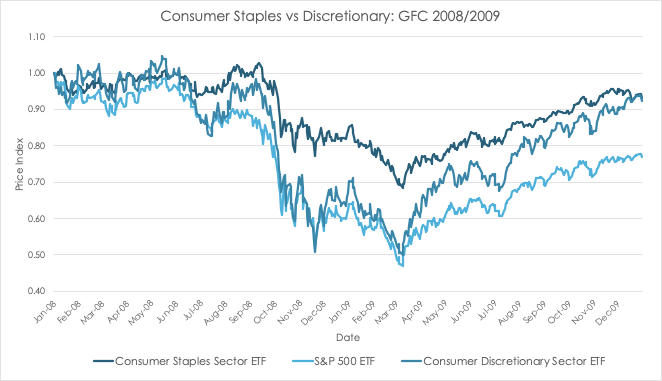

Consumer staples companies, including CPG brands, are typically more stable and more resilient in tough periods for the economy. During the Great Financial Crisis (GFC) of 2008/2009, the share prices of consumer staples companies fared significantly better than those of both consumer discretionary companies (watches, luggage, travel) as well as the broader market, represented by the S&P 500.

In an economic crisis, consumers generally cut back on large ticket items such as vacations, electronics and automotive purchases before they limit their consumption of basic supplies for their homes, families and pets. In addition, BLS data shows that from 2006–2009 there was a 3% increase in meals eaten at home. When people have less disposable income, they spend less money eating out, which leads to the purchase of more CPG staples. More here on how we are able to combine the relative stability of CPG with our data-driven approach to investing to generate strong returns, even during a recession.

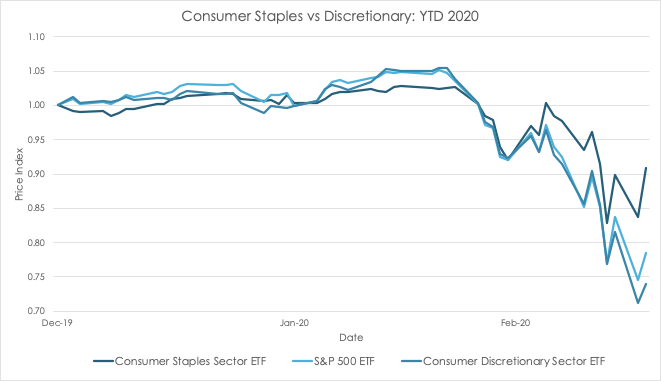

Thus far in 2020, publicly traded consumer staples companies have again demonstrated their defensive nature, drawing down roughly half as much as discretionary sectors and the broader market as the economy continues to wane. Especially in the current environment – with social distancing the new normal – we suspect the durability of CPG staples will only be reinforced by the fact that restaurants are closed and most of the US population will be eating at home until the pandemic is contained.

What Should We Expect From Emerging Brands in a Downturn?

The secular tailwinds over the last 15 years favoring emerging consumer brands (and corresponding headwinds for established brands) have been very strong, as the once considerable barriers to entry in the CPG space have increasingly come down. Historically, distributing through large retailers required high upfront costs, but with the introduction of e-commerce and the elimination of offline slotting fees in some cases, it has become easier to get products on a shelf (digital or physical). Similarly, what were once fixed marketing costs have become more variable through targeted campaigns facilitated by online marketing platforms. Finally, consumer tastes continue to fragment, driving demand for a broader range of products.

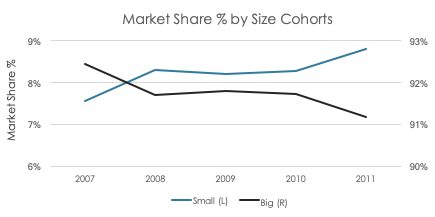

We believe these tailwinds will long outlive the forthcoming downturn. During the last recession beginning in 2008, the then-nascent shift from established brands to emerging brands was barely impacted by the economic backdrop, as consumers persisted in opting for newer brands with innovative products. We can see this by looking at a sample of retail scanner data spanning 35k stores. We found that between 2007–2011, large brands (>$20M revenue) actually lost market share while small brands (<$20M revenue) gained market share.

Since the GFC, the shift to emerging brands has only accelerated as offline retailers have been forced to compete with online distribution models. To increase store traffic, retailers look to win customers by offering a broader assortment of emerging brands than their competition. With such tight margins, retailers can’t afford to simply compete on price. As such, market share continues to shift from big-CPG incumbents who struggle to drive innovation for the consumer. Such trends have been accelerating over the last decade and we believe retailers will continue to address these shifts in consumer preferences, even through a recessionary period. Based on our conversations with senior executives at several retailers, we expect them to remain focused on assortment in order to avoid competing exclusively on price, which is a race to the bottom that they cannot afford in uncertain economic times.

That said, buying behavior may not be perfectly straightforward in the coming weeks and months for emerging brands. In some categories, the main offline retailers are closed by government order. Meanwhile, for brands distributed in “essential” retail outlets, there are still a few challenges that some emerging brands will confront. However, we also anticipate certain opportunities for brands to grow and strengthen their customer base.

First, manufacturers may be pressured to emphasize the top one or two products in each category (typically owned by incumbents) so as to meet the very significant increases in demand in certain core CPG categories. This may leave emerging brands unable to adequately fill new purchase orders. In addition, many retailers have largely postponed any shelf resets, which will delay the opening of new doors for some emerging brands, but will potentially bring opportunity for brands in their existing doors. Shortages in the core products of incumbent brands will lead some consumers to turn to emerging brands’ products as they seek replacements for out-of-stock SKUs – a “free” new channel for customer acquisition.

Further, some emerging brands fall into the premium price bucket for their category and may lose share in a recession as consumers trade down. As a counterpoint, industry sources believe interest in better-for-you and better-for-environment products will endure – brands with a value prop beyond simply being premium (like organic, all natural, cruelty-free etc.) can still differentiate themselves and maintain a loyal customer base.

Needless to say, these potential outcomes will all warrant careful monitoring on a brand-by-brand basis as the crisis evolves.

What Are We Seeing Thus Far?

CPG categories will behave differently in times of economic stress. Given the idiosyncratic nature of the current environment – and a seemingly inevitable and severe recession – we expect shifts in consumer behavior to drive very disparate outcomes across categories. In some cases, demand is already rising dramatically, while for others, distribution channels and supply chains are under enormous strain. The situation is evolving rapidly; however, here are some of our observations thus far:

Pet Products – Not surprisingly, sales have held up well given the longer term trend toward the humanization of pets and their centrality to people’s home life. This has historically proven to be a recession-resistant category, as sales actually increased during the last two recessions. We expect this trend of pet owners investing in pet health and care to continue through a downturn. Much of our portfolio’s pet exposure is online, which we see as a near-term benefit as consumers focus on reducing exposure to trafficked retail locations.

Alcohol – Another category that is likely to be somewhat recession-proof, as it has been in prior recessionary environments. The question will be whether gains from increased home consumption will replace losses from shuttered bars and restaurants. The hit to sales will be particularly felt by brands that operate their own retail locations, such as craft beer taprooms, which are closing due to social distancing measures.

Apparel – Apparel is likely to suffer as a more discretionary category. Initial data points to significant drops in store traffic already that is not likely to be replaced by online sales, as the current impasse in global business will continue to tighten consumer wallets as the crisis unfolds. Our portfolios are exposed to the direct selling channel in apparel, which we suspect will be hit disproportionately hard given the reliance on face-to-face meetings. While only a small proportion of our equity and credit portfolios are exposed to this category (5% and 6%, respectively), we will continue to work closely with our apparel brands in efforts to mitigate the impact of softened discretionary spending.

Personal Care and Beauty – The closing of retail chains such as Sephora and Ulta will prove challenging to brands in this segment of the market. Overall, beauty remains a relatively low price point sector and has proven to be recession-resistant historically; however, we are in an unprecedented time with the level of store closures currently underway. We are advising the entrepreneurs we work with to hone their digital messages with consumers and to focus on direct sales through their own websites. But, it is reasonable to assume sales will still be impacted. Target is one of the last remaining outlets for consumers to purchase cosmetics in-store, which is a positive for some of our companies whose products are sold there. On the plus side, there is a meaningful opportunity for emerging beauty brands with a strong online presence to gain market share.

Food and Non-Alcoholic Beverages – This is – not surprisingly – a category that is thus far proving to be counter-cyclical and a “beneficiary” of the crisis. We have all seen pictures of empty store shelves, extreme delays in online delivery due to excess demand, and dramatic spikes in early sales figures for items like oat milk and take-home meals. While there will be some de-stocking at some point, we remain confident that this category overall will continue to perform, as it has in previous recessions.

Portfolio Snapshots

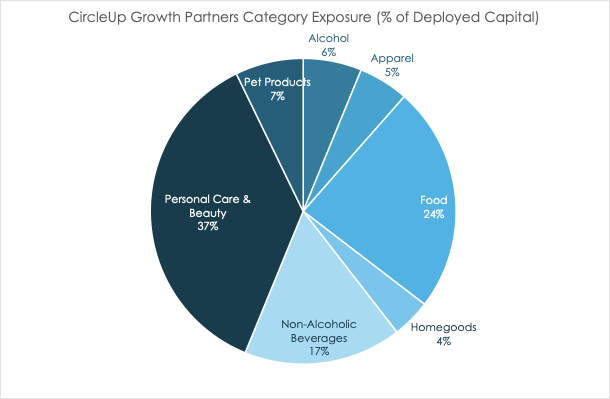

The CircleUp Growth Partners (CGP) equity portfolio has thus far made investments into 20 early-stage CPG companies and is allocated across the main product categories. Our largest exposures are to Food & Beverage (47%) and Personal Care & Beauty (37%).

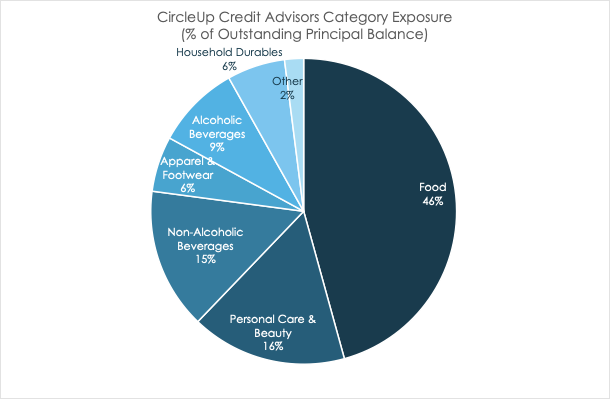

CircleUp Credit Advisors currently has over 100 borrowers, which are spread across categories. Our largest exposure is to Food (46%), followed by Combined Beverages (24%) and Personal Care & Beauty (16%). With 70% of our portfolio in Food & Beverage, we are comforted that we are well-positioned to navigate this challenging market environment. In addition, this cushion allows us to dedicate time and resources to working with companies that are in categories that have been more challenged by recent events.

We are also vigilantly tracking our indirect exposure to retailer performance. Through Helio, we have proven that offline distribution is a leading indicator of future growth for CPG brands. Our portfolio companies, both equity and credit, are dependent on offline distribution within retail outlets such as grocery stores and pharmacies. From a risk management perspective, it is therefore important to monitor how our portfolios are exposed to any given retailer.

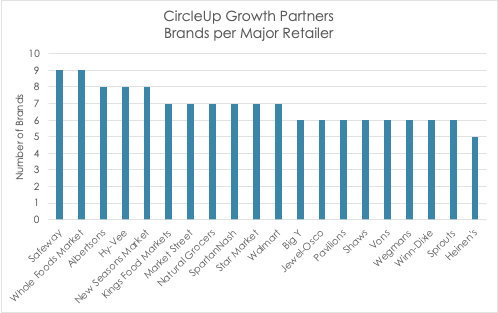

Within our CGP equity portfolio, our brands are distributed across approximately 130 retailers across the US. As shown in the figure below, our largest exposure is to Safeway, which carries just under half of our portfolio’s brands. However, the distribution is fairly even across the US retail sector.

The recent closure of many retailers does impact our portfolio. A couple of our personal care and beauty companies have meaningful exposure to the likes of Sephora and Ulta, and we are actively engaged with those companies to support them in maximizing their distribution through online channels. However, due to our focus on CPG, we have very little exposure to brands that are sold in retailers that are focused primarily on discretionary companies.

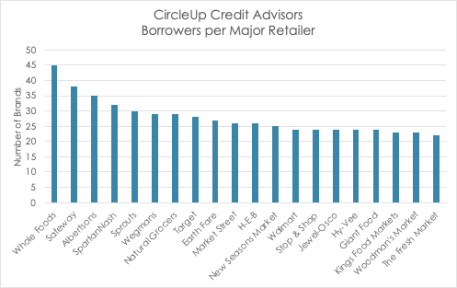

The brands in our credit portfolio sell their products in approximately 170 different retailers across the US. The figure below shows how our credit strategy is also diversified across an array of major retailers. Our largest exposure is to Whole Foods Market, which carries 45 of our portfolio’s brands, representing less than half of the total number of our borrowers.

In addition, a large percentage of our loans are backed by accounts receivable (AR). The payors on these loans are typically large “tier 1” retailers and wholesalers who have stable and well-capitalized balance sheets – most of whom are seeing a meaningful uptick in their business at the moment.

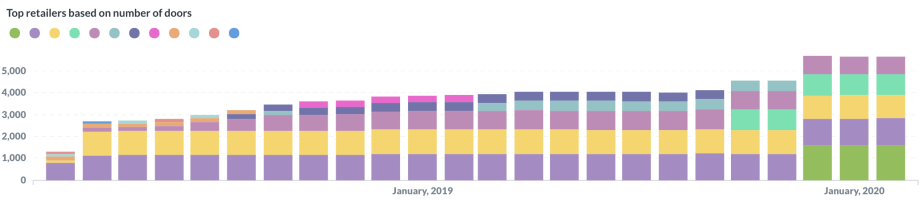

While all of this does give us a certain measure of comfort, it will be very important to continuously monitor the ability of individual borrowers to make good on their obligations. Our Helio platform will be invaluable in this regard, as it enables us to track distribution trends for each of our brands across various retailers on a month-by-month basis. An example of the evolution in offline distribution for one of our portfolio companies is shown in the following chart.

We Are Here to Support Our Entrepreneurs

We talk a lot about the importance of empathy here at CircleUp – and never has that been more important than now. We have been proactive in reaching out to support our existing partners with guidance, capital and other resources. We remain open to bringing new companies into our portfolios, as we believe emerging brands will continue to gain market share over the long-term despite near-term expectations of an economic downturn.

In terms of our CGP equity portfolio, we have had two term sheets accepted and signed in the month of March. Our newest portfolio companies have had exceptional growth in the previous 12 months and expect continued momentum in their categories, which are experiencing increased demand and have existing distribution in major food and beverage retailers. In addition, we are in active conversations with entrepreneurs around how they can conserve cash and shore up balance sheets, while setting them up for success when the recovery ultimately comes around.

In our credit portfolio, we have seen a combination of companies prudently drawing down their existing lines of credit; however, we also have numerous examples of existing borrowers extending their relationship with CircleUp as they receive very large, new purchase orders. We will continue to provide financing to help these brands meet demand as major retailers cope with supply shortages. We have also seen a few examples of companies who were in the midst of arranging alternative financing when the crisis hit, only to have their lenders pull back. While we have enacted our own enhanced underwriting standards for new borrowers, in some of these cases we have been able to step in to provide the capital that these businesses need.

There is a huge amount of uncertainty at the moment and we intend to keep all of our partners apprised of what the data is telling us, what we are seeing, and how we are finding ways to support entrepreneurs through this extremely difficult period. Please reach out if you have questions for feedback.

Zen Water

A water brand with an estimated revenue of $10-$20M (a +407% YoY increase)

Recess

A carbonated drink brand with an estimated revenue of $10-$20M (a +104% YoY increase)

Mad Tasty

A water brand with an estimated revenue of $1-$5M

Shine Water

A water brand that is in 3,000 retail doors (a +329% YoY increase)

All Wello

A juice brand with an estimated revenue of $1-$5M (a +89% YoY increase)

By understanding how these trends will impact the CPG landscape, you can position your business for success.

To learn more about Helio or get in touch, visit heliodata.com.