At CircleUp, we’re re-imagining the mechanics of investing in early-stage companies through the use of Helio, our machine learning platform. As part of that paradigm shift, we like to think about early- stage investing probabilistically much as investors in public markets have done for decades. In what follows, I’d like to use a bit of statistics to explain how we at CircleUp think about applying probabilistic principles to private investing and to demonstrate how the slightest information advantage can have incredible implications for returns. Spoiler alert: with an information advantage (like Helio) we can increase returns by 45% just by shifting 10% of two return probabilities. It’s no surprise that all funds are looking for that slight advantage.

A typical private investor diligences deals with a binary approach – can the company reach the target return, or not? There is a lot of analysis that goes into building conviction (e.g. market sizing, customer sentiment studies, financial modeling) but it boils down to a yes/no vote, which is forever tied to an individual’s track record. Compare this binary approach to the probability weighted approach taken by hedge funds.

Ray Dalio, founder of the world’s largest hedge fund Bridgewater Associates, writes, “Don’t mistake possibilities for probabilities. Anything is possible. It’s the probabilities that matter. Everything must be weighed in terms of its likelihood and prioritized. People who can accurately sort probabilities from possibilities are generally strong at “practical thinking”; they’re the opposite of the “philosopher” types who tend to get lost in clouds of possibilities.

Why wouldn’t we apply probabilities to venture capital? At CircleUp we do in order to fulfill our mission – to help entrepreneurs thrive by giving them the capital and resources they need – at a much larger scale than ever before. Let’s take a look at how portfolio size, correlation, and information advantage can impact the returns for an early-stage venture capital fund.

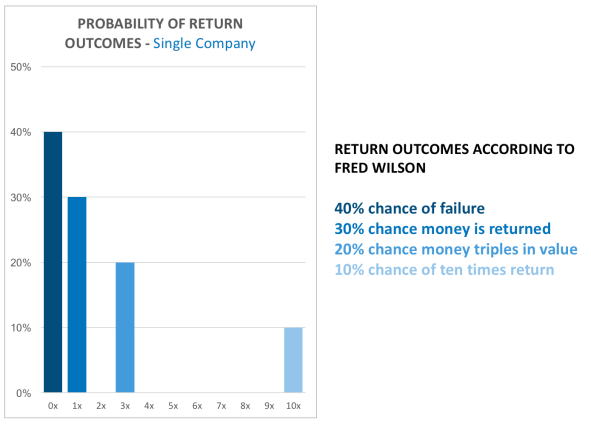

For illustrative purposes, we’ve conducted general analysis based on USV Partner Fred Wilson’s assumed probability of return outcomes for a single investment. In a later post we will go into the specifics of early-stage consumer and retail investing. We know these return outcomes aren’t perfect, but they will help illustrate the key points.

I: IMPACT OF PORTFOLIO SIZE

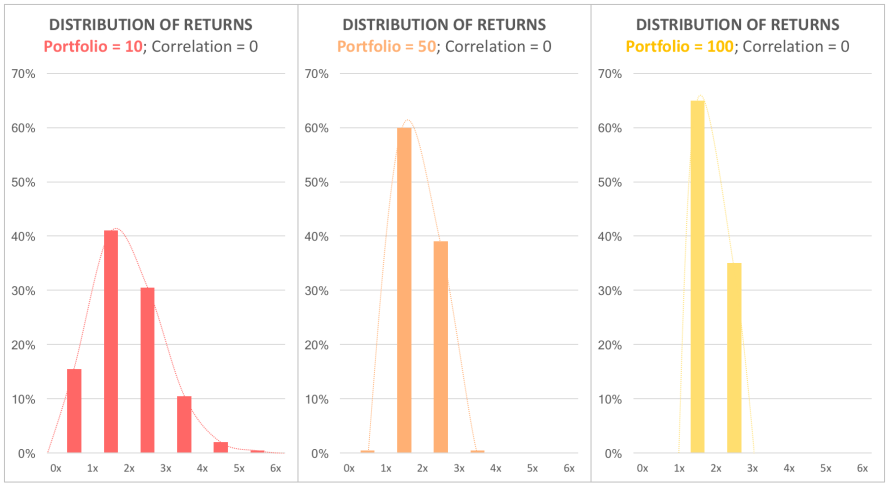

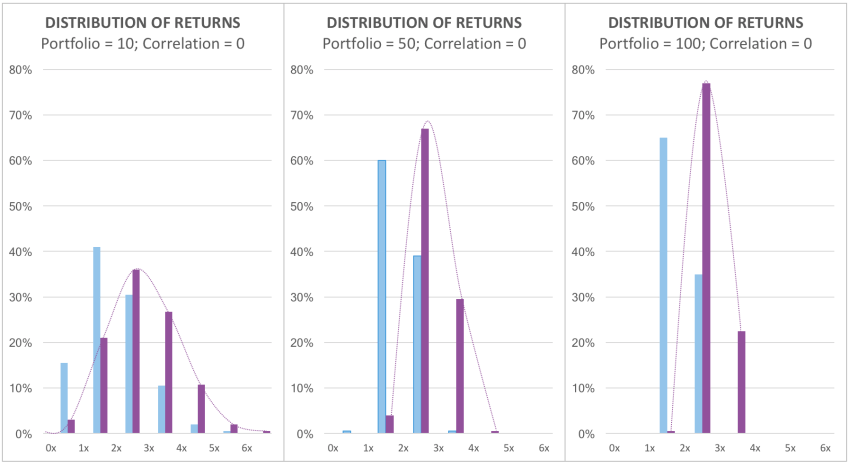

In the sample data, one in ten companies yield a 10x return, while four in ten go to zero. With a portfolio of one, the return outcome mirrors the blue graph above. But if you invest in a portfolio of 10, 50, or 100 companies, the expected distribution of portfolio-level returns begins to narrow. Every individual company has the same expected probability of return outcomes (shown in blue above), but assuming no correlation between the investments in your portfolio, the portfolio-level return expectations become more and more predictable as the number of investments grow:

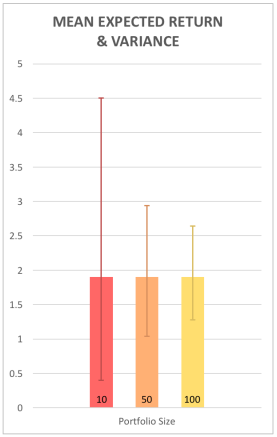

The distribution of outcomes narrows as a portfolio gets bigger. With 100 companies (in yellow), there is a 65% chance that the returns are 1.5x and a 35% chance of 2.5x. Compare that to a portfolio of 10 (in red) where there are many more possible outcomes at smaller percentages. This makes intuitive sense – the more bets you make, the less of an impact the outliers have on the blended results. The mean expected outcome of these three portfolios remain the same at 1.9x Multiple of Money (Mo

M), but the variance from this average diminishes meaningfully. The 10-company portfolio will have a MoM between 0.39x – 4.50x (within 98% confidence band) compared to the 100-company portfolio which will see a MoM between 1.26x – 2.26x (within 98% confidence band). The latter has a much tighter band.

Using Dalio’s framework, it is commonly believed that the role of venture investors is to fund what is possible, and it would be wise to overlay assumptions about what is probable in order to construct a portfolio with the highest possible risk adjusted returns.

Larry Fink, CEO of $6.3 trillion asset manager BlackRock, has described the origins of the firm, “The roots of the organization were founded on the concept of risk management and technology.” CircleUp is extending this approach to the private markets.

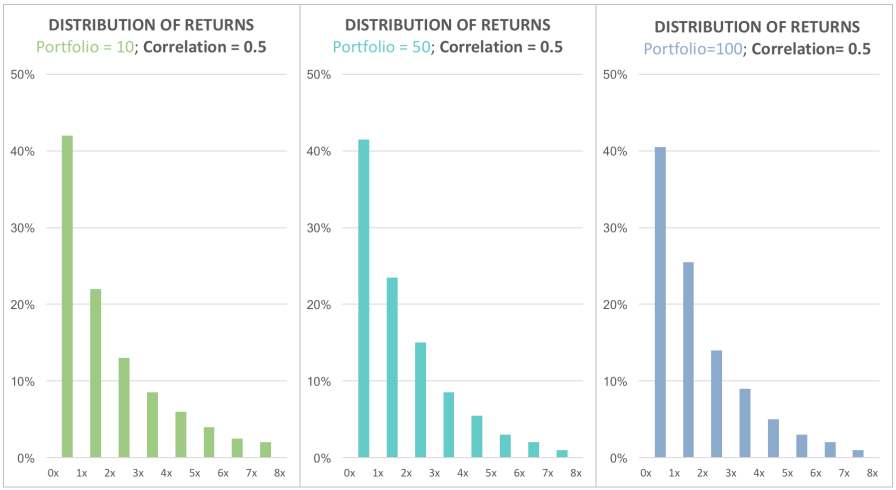

II: IMPACT OF CORRELATION

The analysis above assumes that there is no correlation between the companies in the portfolio. That isn’t realistic – no VC can make the claim that the correlations is truly zero. So what happens when the companies are correlated? What if an investor has a thesis specifically about cryptocurrency or robotics or fiber optics? Here we have applied a correlation coefficient of 0.5 (max of 1, min of -1, to measure how strong a relationship is between two variables) to understand how the lack of independence in a portfolio of bets impacts an early stage venture portfolio:

Again, the mean expected return remains constant, at 1.9x MoM, for portfolios of 10, 50, and 100 companies (other work has shown that there’s a diminishing return to portfolio sizes above an n of 100). But when these bets are correlated, portfolio size doesn’t meaningfully affect the distribution of possible outcomes. This is also intuitive – if an investor bets on a specific category (e.g. self-driving cars), the number of bets doesn’t help to de-risk the success or failure of the category at large.

III: IMPACT OF INFORMATION ADVANTAGE

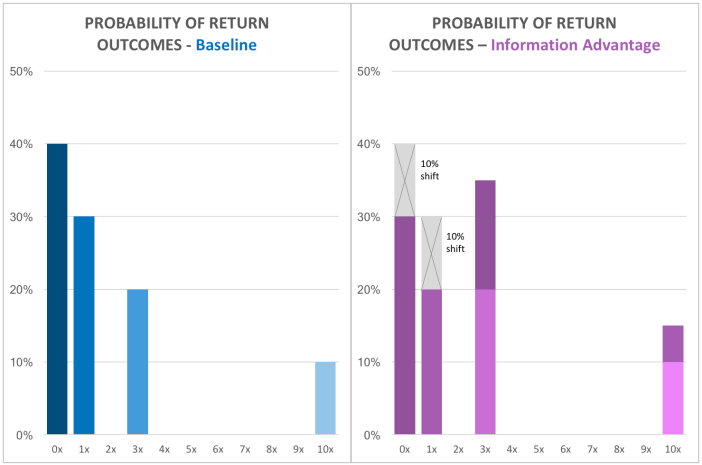

Now for the fun part. Let’s simulate an information advantage that shifts the outcome profile of each company – by reducing the probability of 0X and 1X returns by 10% and increasing the probability of 3X returns from 20% to 35% and increasing the probability of 10x returns slightly from 10% to 15% (blue is baseline, purple is with information advantage):

(At CircleUp, this information advantage comes from our technology called Helio. More to come in following blogs.)

What does this information advantage do for returns? Rather than an average of 1.9x MoM, there is an average of 2.8x MoM. That is a 45% bump in returns (shown in purple vs. the baseline case in blue). This increase in return can be shown at all portfolio sizes:

Most notably, the 100-company portfolio now has an expected 99% chance of exceeding 2.0x returns, a 50% chance of exceeding 2.75x returns and a 25% chance of exceeding 2.97x returns. By combining an information edge and keeping the correlation low in a 100-company portfolio, the math here shows a very compelling return profile. To level set, Cambridge Associates shows that the average Total Value to Paid In Capital Multiple (TVPI) for vintages between 2000-2011(as of 2014) is a multiple of 0.65x. In simple terms, venture investors are losing money, on average.

Intrigued? You will hear more from us on how Helio is being used, not to guarantee success, but to increase the probability in a way that amplifies and de-risks returns. We are not on a mission to be 100% accurate on every bet we make, but we are on a mission to shift the outcomes ever so slightly in our favor. This small information advantage can have an incredibly powerful effect on return outcomes, just as patient history is an information advantage with huge impacts in the medical field. We are on a mission to shift how private investors think about investments – from individual deal binary terms to portfolio-level probabilistic terms.

This article is for informational purposes only and may not be considered a recommendation or investment advice.

Zen Water

A water brand with an estimated revenue of $10-$20M (a +407% YoY increase)

Recess

A carbonated drink brand with an estimated revenue of $10-$20M (a +104% YoY increase)

Mad Tasty

A water brand with an estimated revenue of $1-$5M

Shine Water

A water brand that is in 3,000 retail doors (a +329% YoY increase)

All Wello

A juice brand with an estimated revenue of $1-$5M (a +89% YoY increase)

By understanding how these trends will impact the CPG landscape, you can position your business for success.

To learn more about Helio or get in touch, visit heliodata.com.